Can I Use Land as Collateral for a Loan?

Using land as collateral for a loan is a common practice. It allows borrowers to access larger loan amounts and potentially more favorable interest rates than they might with unsecured loans. However, this type of secured loan also comes with certain risks that borrowers should carefully consider. This article explores the intricacies of using land as collateral, examining the process, benefits, drawbacks, and essential factors to consider before making a decision.

Similar to car loans canada review, secured loans often require a comprehensive understanding of the terms and conditions.

What Does Using Land as Collateral Mean?

Using land as collateral means pledging your property ownership as security for a loan. If you default on the loan, the lender has the right to seize and sell the land to recoup their losses. The land acts as a guarantee for the lender, reducing their risk and making them more willing to lend.

Different Types of Loans That Accept Land as Collateral

Several loan types accept land as collateral, including mortgages, home equity loans, construction loans, and land loans. Each loan type has specific requirements and purposes. For example, a construction loan uses the land as collateral for the funds to build a house on that land, while a land loan is specifically for purchasing land.

Different Types of Loans Accepting Land as Collateral

Different Types of Loans Accepting Land as Collateral

Benefits of Using Land as Collateral

The primary advantages of using land as collateral are access to larger loan amounts and potentially lower interest rates. Lenders view secured loans as less risky, which allows them to offer more competitive terms. This can be particularly beneficial for large purchases or investments.

How Does Land Appraisal Affect Loan Amount?

The appraised value of your land plays a crucial role in determining the loan amount you can secure. Lenders typically lend a percentage of the appraised value, known as the loan-to-value ratio (LTV). A higher appraised value generally translates to a higher loan amount.

Risks of Using Land as Collateral

While using land as collateral can be advantageous, it’s crucial to understand the inherent risks. The most significant risk is losing your property if you default on the loan. This can have devastating financial and personal consequences.

What Happens if I Default on a Loan Secured by Land?

If you default on a loan secured by land, the lender can initiate foreclosure proceedings. This process involves legally taking possession of the property and selling it to recover the outstanding loan balance.

As with title loans enid ok, defaulting on a secured loan can have severe consequences.

Factors to Consider Before Using Land as Collateral

Before using land as collateral, carefully evaluate your financial situation, the loan terms, and the potential risks. Ensure you can comfortably afford the monthly payments and understand the implications of defaulting on the loan.

What are the Legal Implications of Using Land as Collateral?

Using land as collateral involves complex legal agreements. It’s essential to consult with a legal professional to fully understand your rights and obligations before signing any documents. They can help you navigate the legal complexities and ensure you are protected.

Legal Implications of Using Land as Collateral

Legal Implications of Using Land as Collateral

How to Use Land as Collateral for a Loan

The process of using land as collateral typically involves getting the land appraised, applying for the loan, and providing the necessary documentation to the lender. The lender will then review your application and determine the loan terms.

Much like exploring loans kingston, understanding the local regulations and lender requirements is crucial.

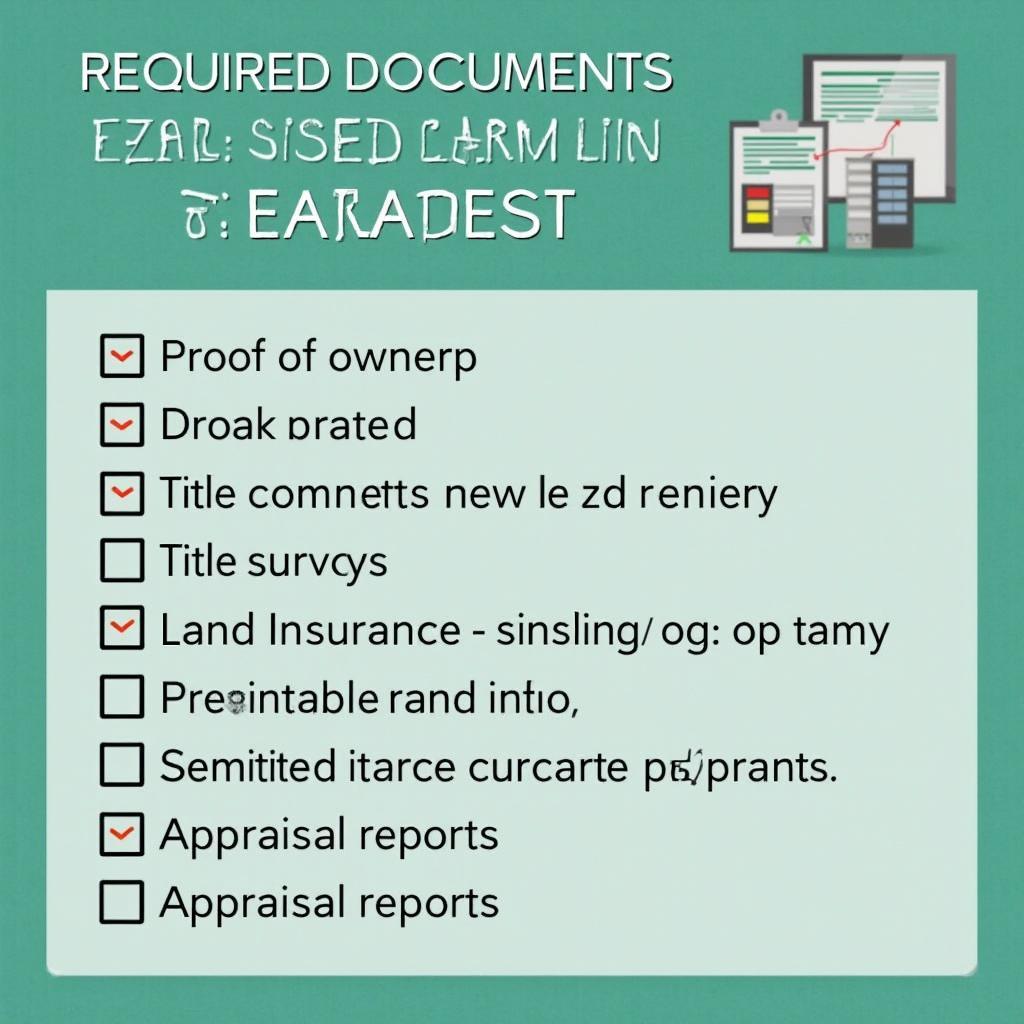

What Documentation is Required to Use Land as Collateral?

Lenders typically require documentation such as proof of ownership, land surveys, title insurance, and appraisal reports. The specific requirements may vary depending on the lender and the loan type.

“Understanding the intricacies of land ownership and loan agreements is paramount before leveraging your property,” says Nguyen Thi Loan, a seasoned financial advisor at ABC Financial Group. “Seeking expert legal counsel is crucial for navigating the process and protecting your interests.”

Required Documentation for Using Land as Collateral

Required Documentation for Using Land as Collateral

Conclusion

Using land as collateral can be a viable option for securing a loan, offering access to larger sums and potentially lower interest rates. However, it also carries the significant risk of losing your property if you default. Carefully consider your financial situation, the loan terms, and the potential risks before making a decision. Thorough research and seeking professional advice are crucial to ensuring you make an informed and responsible choice when using land as collateral for a loan.

For those researching loan options in different regions, resources like loans victoria can offer valuable insights.

FAQ

- What is the loan-to-value ratio (LTV)?

- Can I use land I don’t fully own as collateral?

- How is the value of my land determined?

- What are the alternatives to using land as collateral?

- How can I improve my chances of getting approved for a loan secured by land?

- What are the typical interest rates for loans secured by land?

- What are the tax implications of using land as collateral?

“Evaluating your long-term financial goals and risk tolerance is essential when considering using land as collateral,” advises Pham Van Minh, a senior loan officer at XYZ Bank. “Don’t hesitate to seek professional advice to ensure this strategy aligns with your overall financial plan.”

Considering different loan options? You might find helpful resources like loans for unemployed people in texas.